December 3, 2023

Volume 10, Issue 49

Weekly Recap

Most of the major domestic equity indexes moved higher last week, with the S&P 500 and Nasdaq Composite rounding out on Thursday their best monthly gains (8.9% and 10.7%, respectively) since July 2020. Falling U.S. Treasury yields seemed to continue to boost sentiment, and a broad index of the bond market recorded its best monthly gain since 1985.

Last week also brought more good news on the inflation front. On Thursday, the Commerce Department reported that the Federal Reserve’s preferred inflation gauge, the core (ex-food and energy) personal consumption expenditures price index, rose 0.2 percent in October, a slowdown from September. This brought its year-over-year increase down to 3.5 percent – still well above the Fed’s 2 percent target, but the lowest level since April 2021. Over the past six months, core PCE was running even slower, at an annualized rate of 2.5 percent.

Even before the data release, a noted Fed hawk, Board Member Christopher Waller, surprised traders on Tuesday by telling a Washington conference that, “I am increasingly confident that policy is currently well positioned to slow the economy and get inflation back to 2 percent.” While cautioning that work remained, he also acknowledged that “we have seen the most rapid decline in inflation on record.”

Waller also told the audience that if inflation continued to moderate over the next three to five months, “we could start lowering the policy rate just because inflation is lower,” stressing that “it has nothing to do with trying to save the economy. It is consistent with every policy rule. There is no reason to say we will keep it really high.”

A slight change in tone from Fed Chair Jerome Powell may have helped both stocks and bonds end the week on a strong note. In a speech on Friday, Powell acknowledged that interest rates were now “well into restrictive territory.” He also warned that the Fed would raise rates again, however, if dictated by the data.

Last week arguably offered some evidence that the economy may be headed toward policymakers’ goal of a “soft landing.” Personal spending rose 0.2 percent in September, its smallest increase in six months, while personal incomes rose at the same pace. Housing permits came in above expectations, but actual starts surprised on the downside. Weekly jobless claims ticked down, but continuing claims jumped much more than expected to 1.93 million, their highest level since November 2021.

Hopes that the economy is running neither too hot nor too cold – the so-called “Goldilocks” scenario – may have been boosted by the release on Thursday of the Fed’s Beige Book. The central bank’s periodic survey of economic activity in its 12 separate districts was split down the middle, with half reporting growth and half contraction.

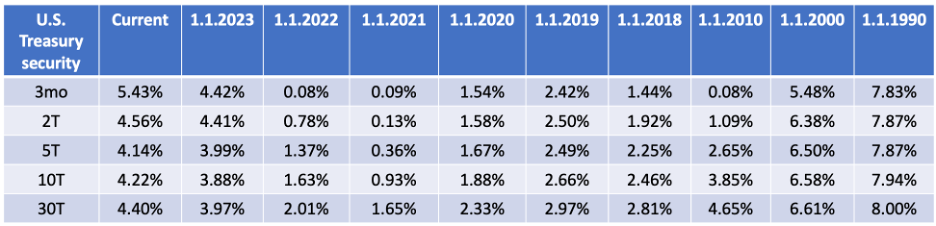

Mr. Powell’s comments helped push the yield on the benchmark 10-year U.S. Treasury note down to nearly a three-month low of 4.21 percent in intraday trading on Friday.

Market Monitor

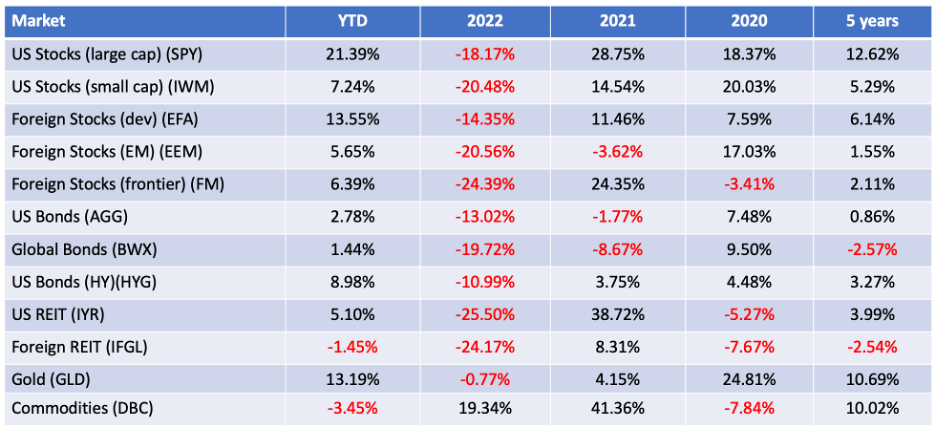

A full listing of market performance data is available here.

DQYDJ.com (“Don’t Quit Your Day Job”) offers helpful investment calculators here, including one that shows total returns for individual stocks.

Koyfin.com provides reams of data on individual stocks, including the ability to track total return — and just about anything else — over time.

In The News

Consumer spending rose 0.2 percent in October, down sharply from a 0.7 percent rise in September, the Commerce Department said Thursday. The October reading marked the slowest increase since May. The combination of ebbing income growth, high interest rates and prices, dwindling pandemic savings and the resumption of student-loan payments is eroding Americans’ ability to keep boosting their spending as briskly as they did through the summer.

Inflation has cooled markedly this year, likely bringing the Federal Reserve’s interest-rate increases to an end. Price growth as measured by the personal-consumption expenditures price index, the Fed’s preferred inflation gauge, remained mild in October.

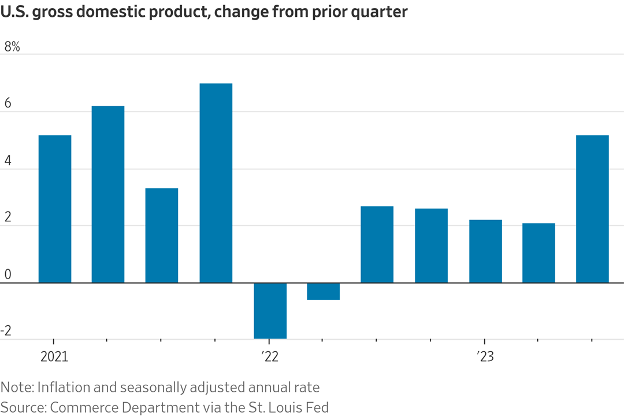

The economy grew faster than previously estimated during the third quarter—at a blistering seasonally- and inflation-adjusted 5.2 percent annual rate – because there was more fixed investment as well as state and local government spending than initially thought, the Commerce Department announced Wednesday. The new figure was revised up from an initial estimate of a 4.9 percent pace. Economists expect growth to slow in the fourth quarter as consumers pull back on spending.

Mortgage rates fell for a fifth straight week, bringing them to the lowest level in more than two months. The average rate on the standard 30-year fixed mortgage declined to 7.22 percent, according to mortgage-finance giant Freddie Mac. Mortgage rates have fallen more than half a percentage point over the past month, the largest four-week decline since late 2022.

Home prices rose to a new record in September due to a shortage of homes for sale, even as high interest rates made home purchases less affordable. The S&P CoreLogic Case-Shiller National Home Price Index, which measures home prices across the nation, rose 3.9 percent from a year earlier in September, compared with a 2.5 percent annual increase the prior month. The September level was the highest since the index began in 1987.

The Conference Board’s Consumer Confidence Index increased in November, bouncing back after falling for three straight months. But a measure of consumer expectations remained below 80 (at 77.8) for the third month in a row. According to the business group, levels below that threshold signal a recession within the next year.

Twenty months after the Federal Reserve began a historic campaign against inflation, investors now believethere is a much greater chance that the central bank will cut rates in just four months than raise them again in the foreseeable future.

Despite wage increases, more paid time off and greater control over where they work, the number of U.S. workers who say they are angry, stressed and disengaged is climbing, according to Gallup’s 2023 workplace report.

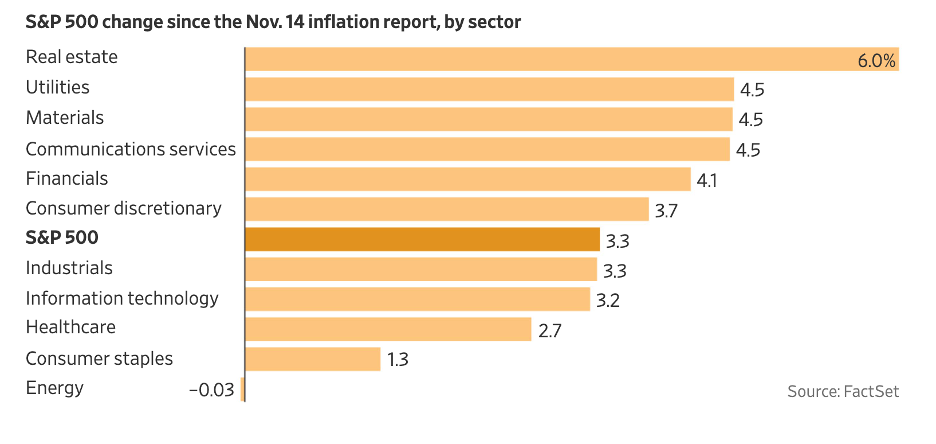

Charts of the Week

Good Reads

I found the following articles to be of note. Some may be of interest only to advisors while others are aimed more broadly. You may hit paywalls below; most can be overcome here.

- Macro Outlook 2024: The Hard Part is Over (Goldman Sachs)

- 2024: Prime Time for Bonds (Pimco)

- Four Lucrative Tax Deductions That Seniors Often Overlook (Lori Ioannou)

- Three Retirement Income Crises Are Brewing (Ric Edelman)

This is the best thing I read last week. The sweetest. The most terrifying. The most significant. The least surprising. I loved this. Anne Lamott on aging. RIP, Charlie Munger. RIP, Douglass North. Lincoln’s 1863 Thanksgiving Day address. A statistical puzzle: How many people do you know? McDonald’s is getting less efficient … on purpose. What if you met your future self? The 100 greatest BBC music performances – ranked! How the mighty have fallen.

With an average age of 78, the Rolling Stones are hitting the road again in 2024 with a 16-city tour. It is being sponsored by AARP (really).

“A good bet in economics: the past wasn’t as good as you remember, the present isn’t as bad as you think, and the future will be better than you anticipate.”~Morgan Housel

Securities and advisory services are offered through Madison Avenue Securities, LLC, a member of FINRA and SIPC, a registered investment advisor.

This report provides general information only and is based upon current public information we consider reliable. Neither the information nor any opinion expressed constitutes an offer or an invitation to make an offer, to buy or sell any securities or other investment or any options, futures, or derivatives related to such securities or investments. It is not intended to provide personal investment advice and it does not take into account the specific investment objectives, financial situation, and the particular needs of any specific person who may receive this report. Investors should seek financial advice regarding the appropriateness of investing in any securities, other investment, or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investors should note that income from such securities or other investments, if any, may fluctuate and that price or value of such securities and investments may rise or fall. Accordingly, investors may receive back less than originally invested. Past performance is not necessarily a guide to future performance. Diversification does not guaranty against loss in declining markets.