February 18, 2024

Volume 11, Issue 7

Weekly Recap

Some favorable earnings surprises balanced against discouraging inflation data left the major domestic equity benchmarks mixed last week, with the S&P 500 recording its first weekly decline since the start of the year. The declines were concentrated in large-cap growth stocks, however, with an equally weighted version of the S&P 500 reaching a record intraday high on Thursday. After suffering its biggest daily drop since June on Tuesday, the small-cap Russell 2000 rebounded to lead the gains for the week.

Several upside inflation surprises were significant last week. On Tuesday, the major indexes sold off after the Labor Department reported that consumer prices had risen 0.3 percent in January, a tick above consensus expectations of around 0.2 percent. More concerning was the 0.4 percent rise in core consumer prices, keeping the year-over-year rise at 3.9 percent, nearly double the Federal Reserve’s 2 percent target.

Stocks regained some momentum on Wednesday, after Chicago Fed President Austan Goolsbee told a conference in New York that slightly higher inflation over the coming months was still consistent with the path back to the Fed’s 2 percent inflation target. He noted that the upside surprises were driven largely by shelter costs (as measured by owners’ equivalent rent), which he termed a “puzzle,” according to Bloomberg. He also cautioned the impact of overtightening on the Fed’s employment mandate.

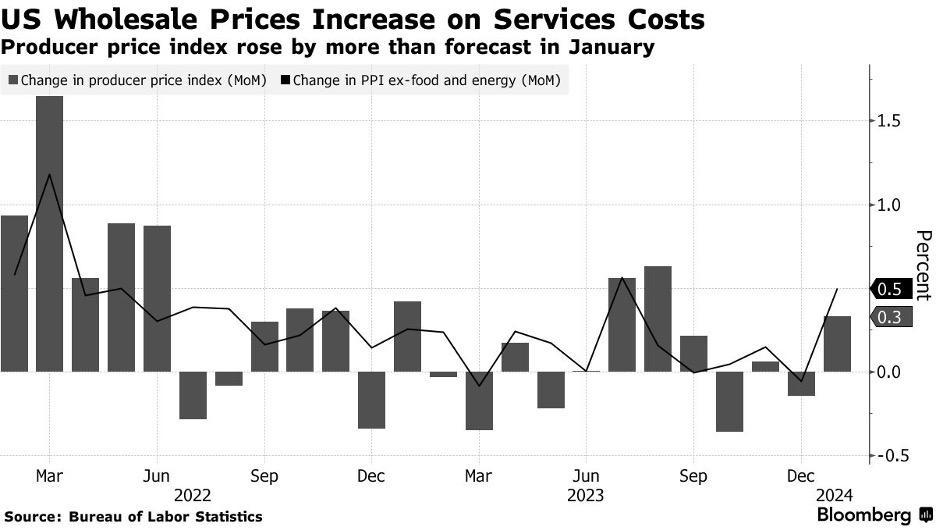

Stock futures fell again after some more substantial upside inflation surprises arrived Friday morning, however. The Labor Department reported that producer prices, which are typically more volatile, had increased 0.3 percent in January – the most in five months – after falling 0.1 percent in December. Core prices rose 0.5 percent, well above expectations of around 0.1 percent. A 2.2 percent jump in the cost of hospital outpatient care was partly to blame.

Much of the rest of last week’s economic data were also arguably disappointing, although signs of weaker growth seemed to help calm inflation concerns. On Thursday, the Commerce Department reported that retail sales had plummeted 0.8 percent in January. While many economists pointed to seasonal factors and harsher weather in January as a reason for the weakness, typically weather-sensitive sales at restaurants and bars rose 0.7 percent. Initial jobless claims also came in below consensus, while continuing claims were slightly above. While housing starts, reported Friday, came in lower than expected, a gauge of homebuilder confidence surprised on the upside.

The inflation data caused many to lower their expectations for potential rate cuts considerably. According to the CME FedWatch Tool, the futures market ended last week pricing in only a 10.5 percent chance of a rate cut in March compared with a 65.1 percent chance a month earlier. The yield on the benchmark 10-year U.S. Treasury note also surged to an intraday high of 4.33 percent on Friday, its highest level since December 1.

Market Monitor

A full listing of market performance data is available here.

DQYDJ.com (“Don’t Quit Your Day Job”) offers helpful investment calculators here, including one that shows total returns for individual stocks.

Koyfin.com provides reams of data on individual stocks, including the ability to track total return — and just about anything else — over time.

In The News

The Consumer Price Index rose 0.3 percent month-over-month and 3.1 percent annually in January, the Bureau of Labor Statistics reported Tuesday, up from 0.2 percent and down from 3.4 percent in December, respectively – and slightly above economists’ expectations. High housing costs were one of the largest factors in the report, and stocks tumbled yesterday as the data seemed to increase the odds that the Federal Reserve will hold interest rates steady at its meeting next month rather than beginning to lower them. Indeed, Federal Reserve officials have been dismissive of market expectations of an imminent rate cut.

Prices paid to U.S. producers rose in January by more than forecast, fueled by a sizable jump in costs of services and highlighting the sticky nature of inflation. The producer price index for final demand increased 0.3 percent from December, Labor Department data showed Friday. The gauge rose 0.9 percent from a year earlier, also exceeding forecasts. The core PPI, which excludes volatile food and energy categories, climbed 0.5 percent from the prior month, and 2 percent from a year ago – both topping expectations.

The number of Americans filing new claims for unemployment benefits fell slightly more than expected last week, pointing to underlying labor market strength despite a recent surge in announced layoffs, mostly in the technology industry.

Janet Yellen is “loath” to make too much of the month-to-month price gyrations, touting progress toward the Fed’s 2 percent inflation target.

Weak demand for office space is squelching appetite for new developments as remote work and high interest rates find ground in major U.S. cities. Among 12 business centers, the decline is particularly steep in Chicago, where nine construction cranes were operating as of August compared with 29 pre-pandemic. Only Manhattan did worse.

Factory production decreased in January for the first time in three months, pointing to a loss of momentum. Weekly jobless claims also unexpectedly declined.

U.S. retail sales broadly declined in January, indicating consumers took a breather after a strong holiday shopping season. The value of retail purchases, unadjusted for inflation, decreased 0.8 percent from December after a downward revision to the prior month, Commerce Department data showed Thursday. The drop was the biggest in nearly a year.

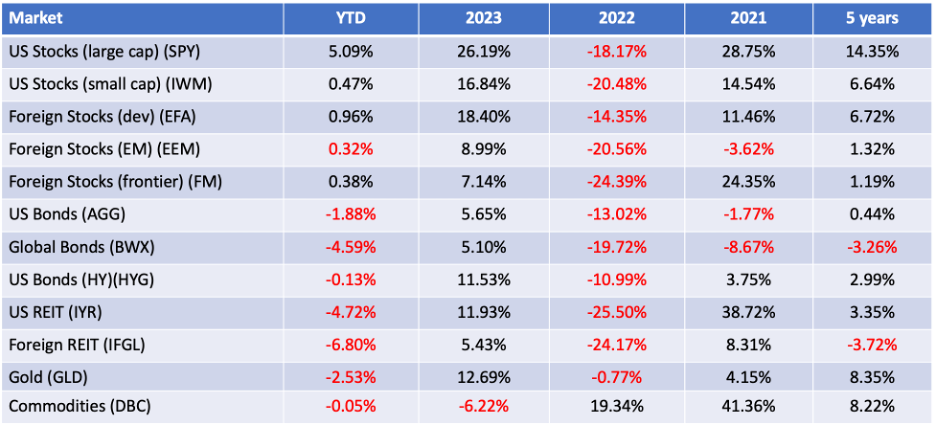

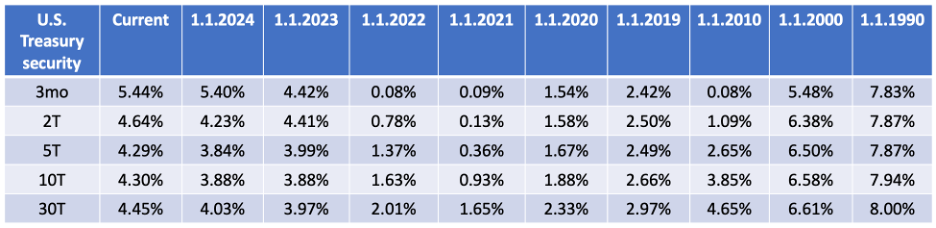

Charts of the Week

Good Reads

Our 2024 Investment Outlook is now available.

I found the following articles to be of note. Some may be of interest only to advisors while others are aimed more broadly. You may hit paywalls below; most can be overcome here.

- There is no holy grail of investing (Tadas Viskanta)

- How to Use Real Estate in Your Portfolio (Amy Arnott)

- These Families Are Shutting Down the Bank of Mom and Dad (Veronica Dagher)

- 12 Filing-Season Tax Facts for 2024 (John Manganaro)

This is the best thing I read in the last week. The most important. The best video. The best writing. Fascinating. Important invention. Lovely. Singers. Warthog. Ya think?! How much snow? On lesson-learning. Quite the romantic. He Gets Us.

After decades of using Valentine’s Day as an opportunity to drive up the dollar value of romance, hotels have turned to a new idea: capitalizing on heartbreak. Consider the Logan Hotel in downtown Philadelphia, which will print your ex’s photo onto a punching bag for you in a private fitness class. That’s just one part of the property’s new $500 Romance Detox package, which includes meditation and spa sessions, but not an overnight stay (which can be added – for an additional fee, of course).

“We cast a shadow on something wherever we stand.”

~ E.M. Forster

Securities and advisory services are offered through Madison Avenue Securities, LLC, a member of FINRA and SIPC, a registered investment advisor.

This report provides general information only and is based upon current public information we consider reliable. Neither the information nor any opinion expressed constitutes an offer or an invitation to make an offer, to buy or sell any securities or other investment or any options, futures, or derivatives related to such securities or investments. It is not intended to provide personal investment advice and it does not take into account the specific investment objectives, financial situation, and the particular needs of any specific person who may receive this report. Investors should seek financial advice regarding the appropriateness of investing in any securities, other investment, or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investors should note that income from such securities or other investments, if any, may fluctuate and that price or value of such securities and investments may rise or fall. Accordingly, investors may receive back less than originally invested. Past performance is not necessarily a guide to future performance. Diversification does not guaranty against loss in declining markets.