March 10, 2024

Volume 11, Issue 10

Weekly Recap

Growing expectations that the Federal Reserve might begin cutting interest rates sooner rather than later powered the S&P 500, S&P MidCap 400, and the Nasdaq Composite to new record intraday highs before pulling back late Friday. Small-cap and value shares outperformed, while mega-cap tech shares lagged due in part to a decline in Apple following reports about slowing iPhone sales in China. Notably, Danish pharmaceuticals company Novo Nordisk, which has seen robust demand for its diabetes and weight loss drugs, displaced Tesla on Thursday as the 12th biggest public company by market capitalization.

Last week began on a down note. On Tuesday, the S&P 500 fell by more than 1 percent for the first time since mid-February, in part due to disappointing policy news out of China. Stocks regained momentum at midweek, however, seemingly on the back of easing demand and inflation pressures domestically.

On Wednesday, the Fed reported in its periodic Beige Book survey of regional economic conditions that consumers were showing more sensitivity to rising prices, while the Labor Department announced that job openings fell in January to their lowest level in three months. The quits rate – the share of workers leaving jobs voluntarily, typically considered a good measure of workers’ perception of the ease of finding a new job – also fell to its lowest level since August 2020, early in the rebound from the pandemic.

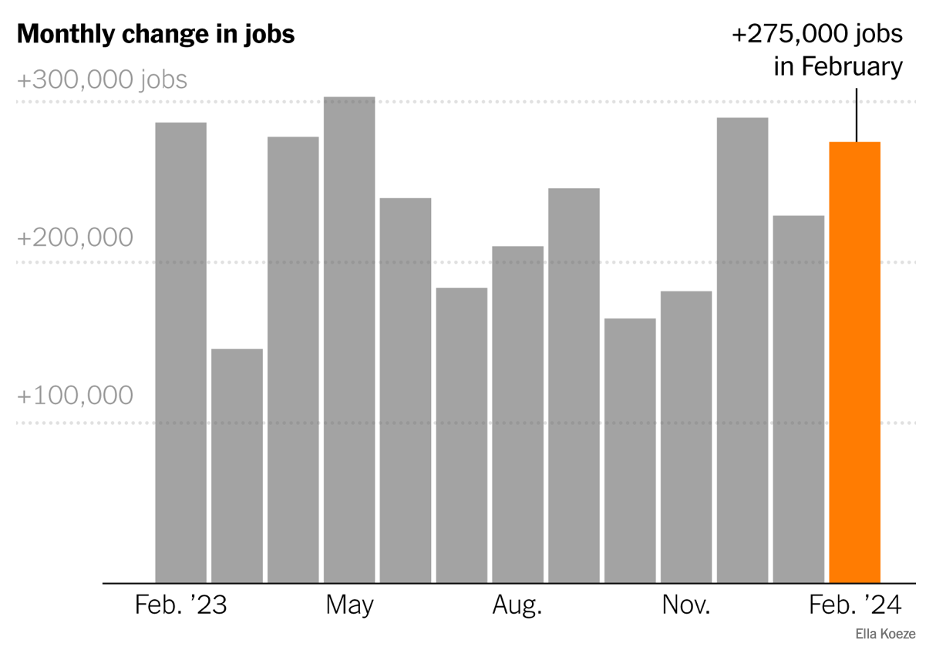

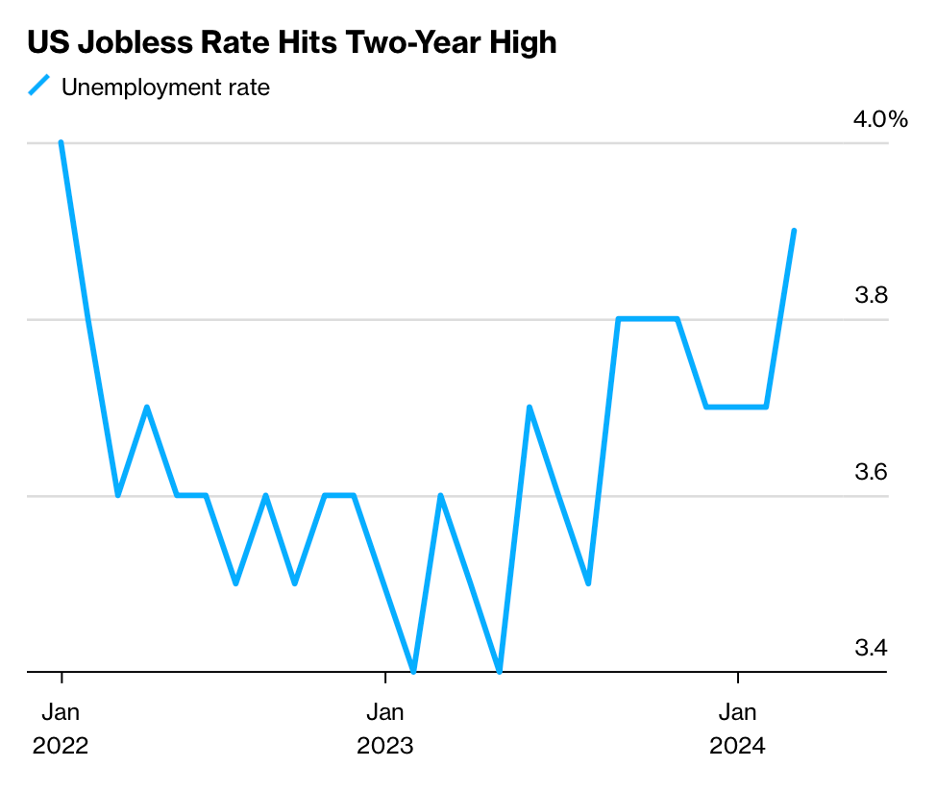

Friday’s jobs report also seemed, at least initially, to reassure investors about the labor market. Employers added 275,000 jobs in February, more than consensus forecasts of around 200,000, but January’s gain was revised significantly lower, from 353,000 to 229,000. Moreover, the unemployment rate rose unexpectedly from 3.7 to 3.9 percent, its highest level in over two years. In a positive sign for inflation, average hourly earnings rose 0.1 percent, below expectations and down sharply from January’s 0.5 percent increase.

Fed Chair Jerome Powell testified before Congress at midweek. While the testimony was largely seen as reiterating previous Fed talking points, it did offer some less hawkish takeaways on the timing of the path of rate cuts. In particular, Mr. Powell stated that policymakers were “not far” from having the confidence that inflation’s downtrend will be sustained, enabling them to begin cutting rates. As a result, futures markets ended the week pricing in a somewhat higher (71.0 percent, according to the CME FedWatch Tool) chance of a cut at the Fed’s policy meeting by June.

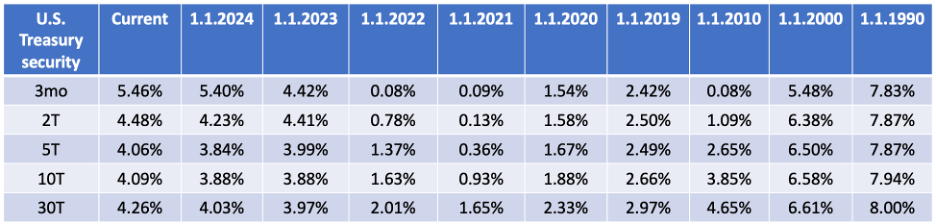

Mr. Powell’s comments and the downside economic surprises helped push the yield on the benchmark 10-year U.S. Treasury note to its lowest intraday level (4.03 percent) since February 2. Gold jumped higher.

Market Monitor

A full listing of market performance data is available here.

DQYDJ.com (“Don’t Quit Your Day Job”) offers helpful investment calculators here, including one that shows total returns for individual stocks.

Koyfin.com provides reams of data on individual stocks, including the ability to track total return — and just about anything else — over time.

In The News

The U.S. jobless rate climbed to a two-year high in February even as hiring remained healthy, pointing to a cooler yet resilient labor market. Nonfarm payrolls advanced 275,000 last month following a combined 167,000 downward revision to the prior two months, the Bureau of Labor Statistics reported Friday. The unemployment rate rose to 3.9 percent and wage gains slowed.

The key takeaway from Fed Chair Jerome Powell’s congressional testimony Wednesday is that the Fed’s battle with inflation isn’t quite over. The central bank is still expected to cut interest rates at some point this year, but Mr. Powell also said officials want more evidence that the recent slowdown in inflation is sustainable. A long-run look at U.S. price levels indeed suggests there’s work still to do.

To understand the U.S. economy, the most important thing you’ll read today might be about bacon cheeseburgers. Prices are surging, yet mom-and-pop businesses can’t make any money from selling them. Just a few years ago, a $16 bacon cheeseburger would have seemed absurd at many U.S. restaurants. But at Chef Zorba’s in Denver, a 78-seat restaurant, they are charging about that much for the classic menu staple. That’s up $5 from just 2018. And yet, even at that price, the owners can’t turn a profit.

The Financial Services Institute and its coalition partners filed an amended complaint Tuesday against the Labor Department’s new independent contractor rule, asking the court to declare the 2024 rule invalid, prohibit its implementation and allows the 2021 independent contractor rule to remain in effect.

Charts of the Week

Good Reads

I found the following articles to be of note. Some may be of interest only to advisors while others are aimed more broadly. You may hit paywalls below; most can be overcome here.

- Regime-Based Investing (Henry Neville)

- SPIVA U.S. Year-End 2023 (S&P Global)

- Global Investment Returns Yearbook 2024 (Dimson, Marsh & Staunton)

This is the best thing I read this week. The most worrisome. The most important. The most absurd. The most remarkable. The most disappointing. The best list. The best thread. Common sense.

From 1965 through 2023, $100 invested in Berkshire Hathaway grew to $4,255,516. The same $100 invested in the S&P 500 over the same period is worth $30,811. That means Berkshire could lose 99.3 percent of its value and only then just match the index over 59 years.

“There will always be bull markets followed by bear markets followed by bull markets.”

~ Sir John Templeton

Securities and advisory services are offered through Madison Avenue Securities, LLC, a member of FINRA and SIPC, a registered investment advisor.

This report provides general information only and is based upon current public information we consider reliable. Neither the information nor any opinion expressed constitutes an offer or an invitation to make an offer, to buy or sell any securities or other investment or any options, futures, or derivatives related to such securities or investments. It is not intended to provide personal investment advice and it does not take into account the specific investment objectives, financial situation, and the particular needs of any specific person who may receive this report. Investors should seek financial advice regarding the appropriateness of investing in any securities, other investment, or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investors should note that income from such securities or other investments, if any, may fluctuate and that price or value of such securities and investments may rise or fall. Accordingly, investors may receive back less than originally invested. Past performance is not necessarily a guide to future performance. Diversification does not guaranty against loss in declining markets.