March 3, 2024

Volume 11, Issue 9

Weekly Recap

The major domestic equity benchmarks ended last week mostly higher, with the Nasdaq Composite joining the S&P 500 in record territory for the first time in over two years. The month also closed a strong February, with the S&P marking its strongest beginning two months of the year since 2019. The week’s gains were also broad-based, with an equal-weighted version of the S&P 500 modestly outperforming its more familiar market capitalization version. YTD, however, the cap-weighted version of the index remains ahead by 409 basis points (4.09 percentage points), reflecting the outperformance of large, technology-oriented growth stocks.

The crucial event of the week in terms of market sentiment appeared to be Thursday’s release of the Commerce Department’s core (ex-food and energy) personal consumption expenditures price index. The index rose 2.8 percent for the 12 months ended in January, in line with expectations, but the report appeared to calm concerns over the Labor Department’s earlier release of its consumer price index, which showed core prices rising by 3.9 percent, above expectations of around 3.7 percent. The core PCE price index is generally considered the Federal Reserve’s preferred gauge of overall inflation pressures.

While stocks jumped on the inflation news, it appeared to have a limited impact on the tone of Fed communications. Twelve Fed policymakers delivered speeches last week, and all seemed to echo the recent narrative that they were in no rush to cut interest rates. Indeed, according to the CME FedWatch Tool, futures markets ended last week pricing in only a slightly higher chance of a rate cut over the next two policy meetings – 24.6 percent versus 23.4 percent the week before.

The rest of last week’s heavy economic calendar surprised modestly on the downside. Most notably, and Institute for Supply Management’s gauge of manufacturing activity came in substantially below expectations, falling from an 18-month high of 49.1 in January back to 47.8 in February. (Readings above 50 indicate expansion.) Durable goods offered a more reassuring picture, however, rising 0.1 percent in the month when the volatile defense and aircraft sectors are excluded. An upside surprise came in February personal incomes, which jumped 1.0 percent in February, the biggest gain in a year.

The reassuring PCE data and downside ISM report helped push the yield on the benchmark 10-year Treasury note to its lowest intraday level since February 13 by the end of last week. U.S. Treasuries also generated positive returns as yields decreased amid a healthily digested Treasury supply concession. Intermediate- and long-term rates fell more than short-term rates.

Market Monitor

A full listing of market performance data is available here.

DQYDJ.com (“Don’t Quit Your Day Job”) offers helpful investment calculators here, including one that shows total returns for individual stocks.

Koyfin.com provides reams of data on individual stocks, including the ability to track total return — and just about anything else — over time.

In The News

The Federal Reserve’s preferred measure of inflation, the personal consumption expenditures price index, showed that prices rose 0.3 percent from December to January, the Bureau of Economic Analysis reported Thursday, up from December’s month-over-month increase of 0.1 percent. The annual increase fell to 2.4 percent in January, down from a 2.6 percent year-over-year increase one month earlier. After stripping out more volatile food and energy prices, core PCE increased at a 0.4 percent rate from December to January, up from 0.1 percent in December, marking the largest growth in the metric in a year. The Federal Reserve’s next meeting is set for March 19 and 20, and central bankers are widely expected to hold interest rates steady as inflation persists.

Which inflation measure matters more?

A barometer of business conditions at American manufacturers fell again in February as orders declined and more workers were laid off, but executives said there were preparing for expansion later in the year. The Institute for Supply Management’s index of manufacturers dropped to a two-month low of 47.8 percent in February from 49.1 percent in the prior month.

A Tuesday email to data “super users” suggested a surge in a measure of rental inflation — which had left analysts puzzled — was due to a shift in underlying calculations, rather than just a rise in prices.

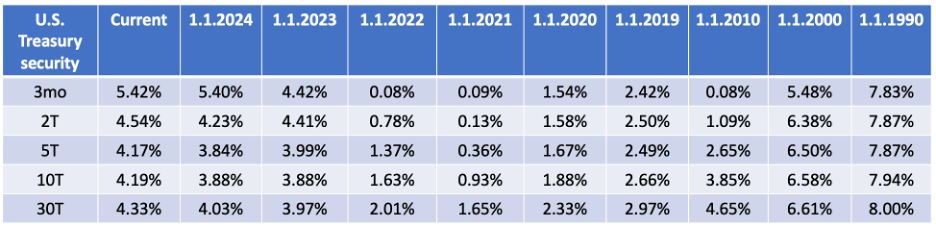

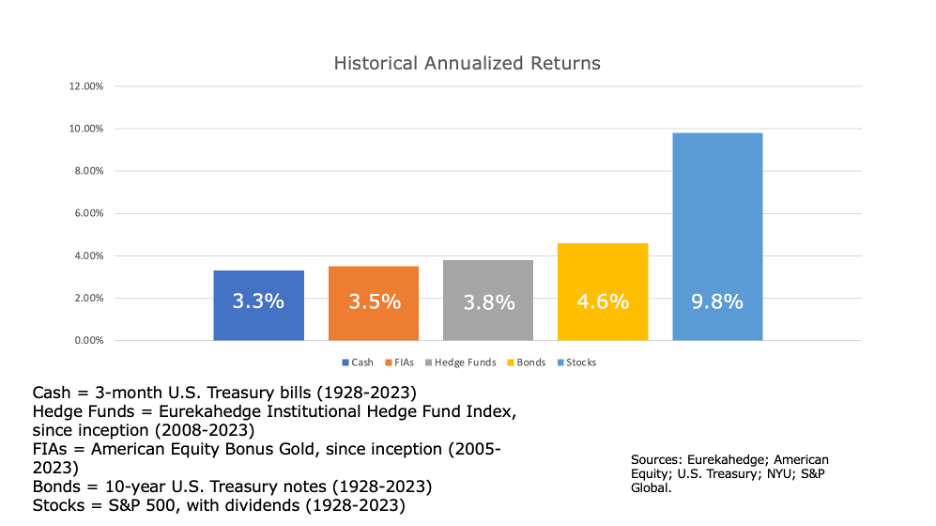

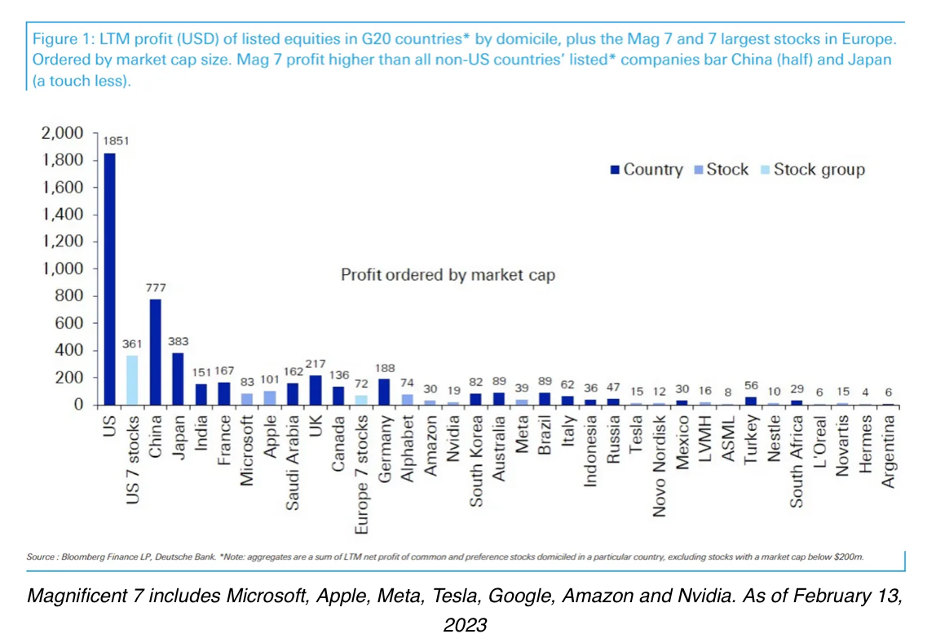

Charts of the Week

Good Reads

Check out the Berkshire Hathaway annual investment letter.

I found the following articles to be of note. Some may be of interest only to advisors while others are aimed more broadly. You may hit paywalls below; most can be overcome here.

- Major Asset Classes | February 2024 | Performance Review

- Magnificent Ignorance about the Magnificent Seven (Owen Lamont)

- What’s the Biggest Risk Right Now? (Ben Carlson)

This is the best thing I read in the last week. The coolest. The sweetest. The wildest. The least surprising. Social engineering at Google. Hmmm.

Nvidia’s market cap is now over $200 billion higher than all of the companies in the S&P 500 Energy sector … combined. Meanwhile, the total net income of the Energy sector is $147 billion versus $19 billion for Nvidia.

“There is nothing which we receive with so much reluctance as advice.”

~ Joseph Addison

Securities and advisory services are offered through Madison Avenue Securities, LLC, a member of FINRA and SIPC, a registered investment advisor.

This report provides general information only and is based upon current public information we consider reliable. Neither the information nor any opinion expressed constitutes an offer or an invitation to make an offer, to buy or sell any securities or other investment or any options, futures, or derivatives related to such securities or investments. It is not intended to provide personal investment advice and it does not take into account the specific investment objectives, financial situation, and the particular needs of any specific person who may receive this report. Investors should seek financial advice regarding the appropriateness of investing in any securities, other investment, or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investors should note that income from such securities or other investments, if any, may fluctuate and that price or value of such securities and investments may rise or fall. Accordingly, investors may receive back less than originally invested. Past performance is not necessarily a guide to future performance. Diversification does not guaranty against loss in declining markets.