November 12, 2023

Volume 10, Issue 46

Weekly Recap

The major domestic equity indexes closed last week mixed, but not before the S&P 500 came close to matching its longest winning streak in nearly two decades. On Wednesday, the S&P notched its eighth straight daily gain, while the Nasdaq Composite marked its ninth. The market’s strength was narrow, however, with an equally weighted version of the S&P 500 lagging its market-weighted counterpart by 190 basis points, and the Russell 1000 Value Index trailing its growth counterpart by 404 basis points – the largest such margin since March.

It was one of the final weeks of major third-quarter corporate earnings releases, and upside surprises from some technology-oriented firms provided support to the growth indexes. Traders noted that high-valuation software stocks seemed to get a general boost from cloud monitoring and security firm Datadog, which surged 28 percent on Tuesday following stronger-than-expected earnings and guidance.

U.S. Treasury debt auctions last week played an uncommonly large role in driving sentiment in both the equity and bond markets. Favorably received auctions of three-year U.S. Treasury notes on Tuesday and 10-year notes on Wednesday were noteworthy.

The initial catalyst in ending the major indexes’ winning streaks, however, appeared to be Thursday’s $24 billion auction of 30-year U.S. Treasury bonds, which was met with the weakest auction demand in two years. Traders have lately been paying close attention to whether demand will be able to keep up with the government’s elevated borrowing needs, particularly in the wake of the temporary lifting of the federal debt ceiling.

There were very few economic data releases last week, and most were in line with expectations. The one exception may have been the University of Michigan’s release on Friday of its preliminary gauge of consumer sentiment, which fell unexpectedly to its lowest level in six months. According to the survey’s chief researcher, the wars in Gaza and Ukraine added to ongoing concerns about higher interest rates. Long-run inflation expectations also reached 3.2 percent, the highest level in the survey since 2011.

U. S. Treasury yields generally decreased through the middle of the week but climbed on Thursday amid the weak 30-year Treasury auction. Traders may have also reacted to comments from Fed Chair Jerome Powell, who told a gathering of the International Monetary Fund that policymakers were “not confident” that they had achieved “a stance of monetary policy that is sufficiently restrictive to bring inflation down to 2 percent over time.” The yield curve flattened.

Market Monitor

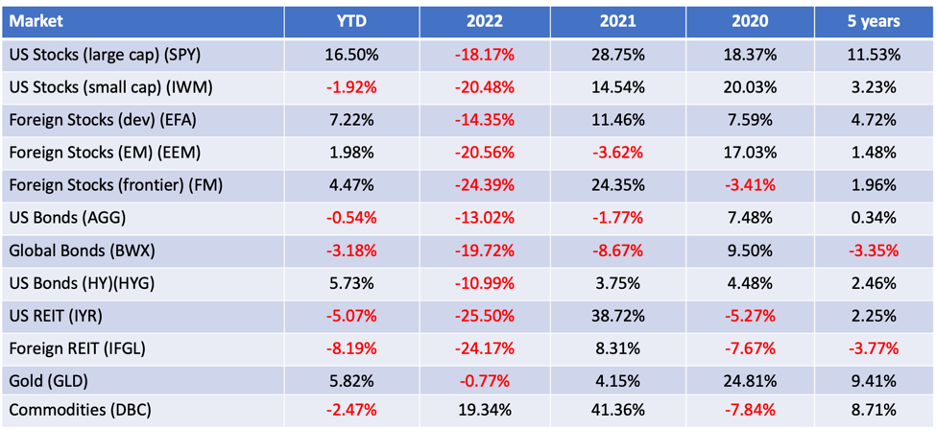

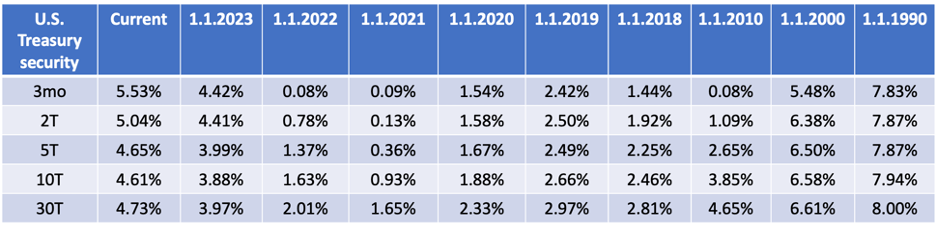

A full listing of market performance data is available here.

DQYDJ.com (“Don’t Quit Your Day Job”) offers helpful investment calculators here, including one that shows total returns for individual stocks.

Koyfin.com provides reams of data on individual stocks, including the ability to track total return — and just about anything else — over time.

In The News

Federal Reserve Chair Jerome Powell indicated the central bank wouldn’t declare an end to its historic interest-rate increases until it had more evidence that inflation was cooling. Price and wage pressures have eased recently, leading more traders to think the Fed is done raising rates. Mr. Powell disappointed them in a speech Thursday by explaining why he thinks the Fed is more likely to tighten policy than ease it. While he didn’t build a case for lifting rates now, Powell pointed to earlier inflation “head fakes,” past episodes in which price pressures ebbed for a while before surprising Fed officials by picking up again.

New projections show that, under the most likely scenario, the U.S. will stop growing by 2080 and shrink slightly by 2100. It is the first time that the Census Bureau has projected a population decline as part of its main outlook for the coming decades.

U.S. consumers’ long-term inflation expectations increased in early November to their highest level since 2011, while (relatively) high interest rates and concerns about the economic outlook weighed on sentiment.

Recurring applications for U.S. unemployment benefits rose for a seventh straight week, adding to evidence that the labor market is cooling. Continuing jobless claims, a proxy for the number of people receiving unemployment benefits, increased to 1.83 million in the week ended Oct. 28, the highest since mid-April, according to Labor Department data out Thursday.

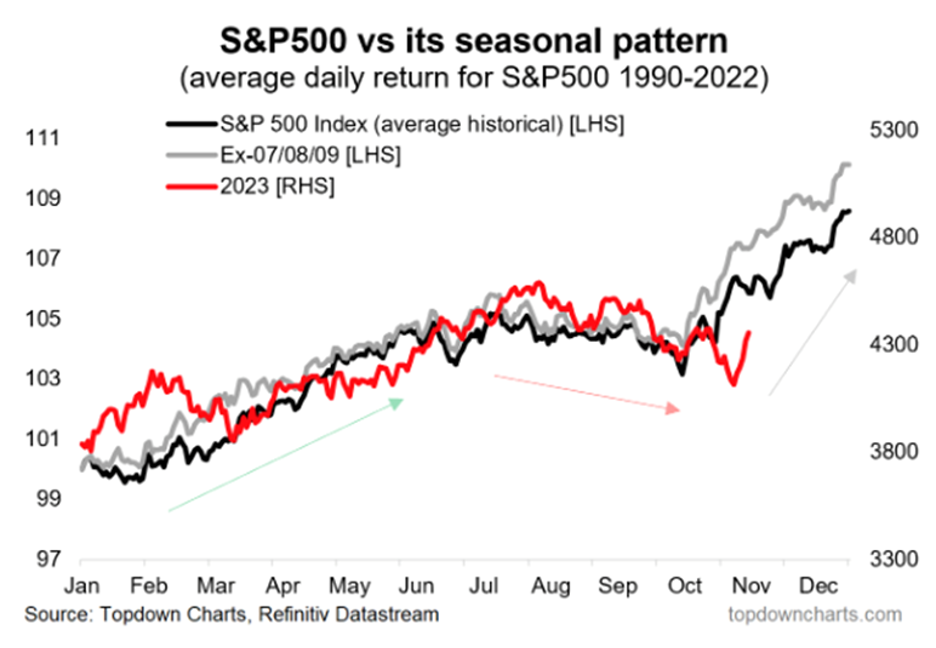

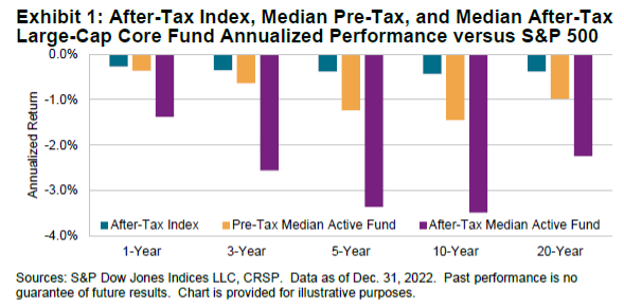

Charts Of The Week

Good Reads

I found the following articles to be of note. Some may be of interest only to advisors while others are aimed more broadly. You may hit paywalls below; most can be overcome here.

- Understanding the proposed Retirement Security Rule

- We Need to Talk About Your Retirement ‘Spending’ (Christine Benz)

- The Fed’s big balancing act (Callie Cox)

This is the best thig I read last week. This is the best thing I watched. The stupidest. The scariest. The saddest. The smartest. The sweetest. The smarmiest. The funniest. The wildest. The most absurd. The most inspiring (unless it was this). The most insightful, (unless it was this). The most predictable. The most addictive. The best thread (unless it was this). Who’s going to tell her? Still wow. Good bureaucracy.

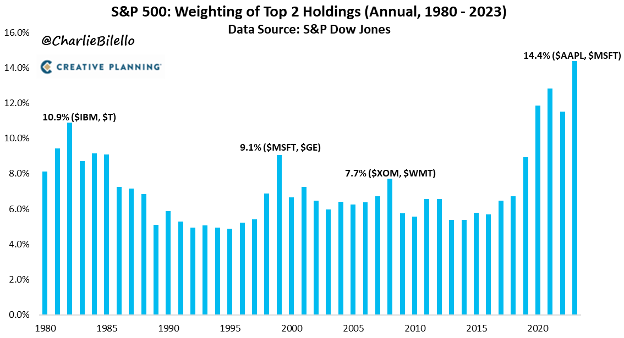

The top 2 stocks in the S&P 500 (Apple & Microsoft) now represent a combined 14.4 percent of the index, the highest weighting for any two companies with data going back to 1980.

Securities and advisory services are offered through Madison Avenue Securities, LLC, a member of FINRA and SIPC, a registered investment advisor.

This report provides general information only and is based upon current public information we consider reliable. Neither the information nor any opinion expressed constitutes an offer or an invitation to make an offer, to buy or sell any securities or other investment or any options, futures, or derivatives related to such securities or investments. It is not intended to provide personal investment advice and it does not take into account the specific investment objectives, financial situation, and the particular needs of any specific person who may receive this report. Investors should seek financial advice regarding the appropriateness of investing in any securities, other investment, or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investors should note that income from such securities or other investments, if any, may fluctuate and