January 11, 2026

Volume 13, Issue 2

Weekly Recap

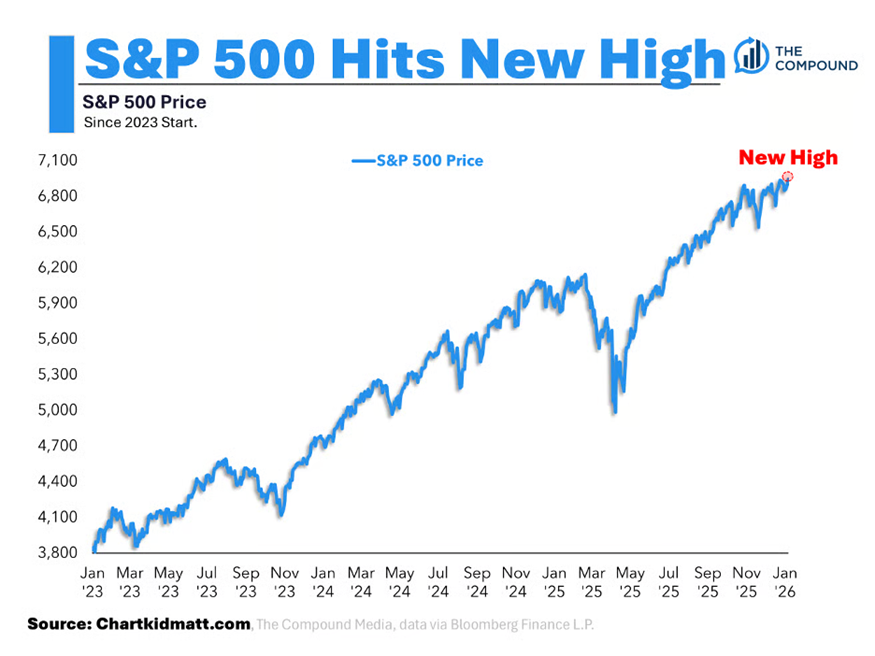

Domestic equities advanced in the first full trading week of the year as traders largely looked past mounting geopolitical tensions, pushing most major indexes to all-time highs. Small-cap and value shares outpaced the large-cap growth stocks that have led returns in recent years, while an equal-weighted version of the S&P 500 outperformed its market cap-weighted counterpart. Of the major indexes, the Russell 2000 performed best, adding a whopping 4.62 percent, while the S&P 500 performed worst but still gained 1.57 percent. Last week also saw several notable industry-level moves in response to a flurry of policy announcements from President Trump. For example, stocks of aerospace and defense companies were hurt on Wednesday by comments that Mr. Trump “will not permit” them to pay dividends or repurchase shares unless they accelerate production of military hardware. The next day, defense stocks rallied after the administration proposed a sizable increase in military spending, as investors priced in the potential for higher government outlays.

Similarly, shares of homebuilders and related industries initially came under pressure after the administration said it would seek to restrict institutional purchases of single-family homes. However, the group rebounded later in the week after Mr. Trump announced that he was instructing government-controlled mortgage companies Fannie Mae and Freddie Mac to buy $200 billion of mortgage bonds to try to drive down lending rates. Credit spreads in the agency mortgage-backed security sector also rapidly tightened on the news.

Last week also brought a heavy dose of economic data releases, including several labor market reports that generally surprised to the downside. Most notably, the Labor Department released its closely watched nonfarm payrolls report on Friday, which showed that U.S. employers added a lighter-than-expected 50,000 jobs in December, while October’s and November’s readings were revised down by a combined 76,000. However, on the more positive side, the unemployment rate ticked down to 4.4 percent from a revised 4.5 percent in the prior month.

The Labor Department’s Job Openings and Labor Turnover Summary for November provided another sign of cooling in the labor market. According to the report, hires declined to 5.1 million for the month, down from 5.4 million in October, while job openings dropped to the lowest level since September 2024 at 7.1 million. Elsewhere, private payrolls processing firm ADP reported that private employers added 41,000 jobs in December, rebounding from a net loss of jobs in the prior month but falling short of estimates for around 47,000 jobs added. Data from the Institute for Supply Management showed that economic activity in the U.S. manufacturing sector contracted for the 10th consecutive month in December, as the ISM’s Manufacturing Purchasing Managers’ Index declined by 0.3 points to 47.9, the lowest reading of 2025 (readings below 50 indicate contraction). The employment index remained in contraction for the 11th straight month, while the prices index stayed in expansion – indicating rising input prices – for the 15th consecutive month.

On the other hand, the ISM’s measure of services activity expanded for the 10th month in a row. Gains in new orders, business activity, and a rebound in employment from contraction to expansion helped push the Services PMI to the highest reading of the year. Price pressures also eased somewhat, although the services prices index remained solidly in expansion territory. U.S. Treasury securities traded slightly higher last week, with some longer-term yields decreasing modestly and short-term yields inching higher. Treasuries rallied early in the week in response to some weaker-than-expected economic data, but follow-through was limited, and trading activity was muted overall. The benchmark 10-year U.S. Treasury note closed last week yielding 4.18 percent.

Market Monitor

A full listing of market performance data is available here.

DQYDJ.com (“Don’t Quit Your Day Job”) offers helpful investment calculators here, including one that shows total returns for individual stocks. Koyfin.com provides reams of data on individual stocks, including the ability to track total return — and just about anything else — over time.

In the News

Employers added 50,000 jobs in December, and the unemployment rate fell to 4.4 percent. But total job gains last year were the weakest since 2020. The report provided the latest in a rapid series of economic updates after several releases were delayed or canceled because of the shutdown. Those glimpses into the state of the economy have demonstrated resilient growth and spending but some softness in the labor market. A new report from payroll company ADP found that the U.S. economy added an estimated 41,000 private sector jobs in December, after reporting a loss of 29,000 jobs in November. Still, manufacturing jobs are difficult to count.

The Commerce Department announced that, in March, the administration will reduce duties on pasta imports for 13 Italian-based producers, cutting total rates from 107 percent to between 17 and 29 percent.

The Chinese-based BYD surpassed Tesla in vehicle sales last year, though Tesla remains the best-selling electric vehicle manufacturer, as BYD sells both plug-in hybrids and battery-electric cars.

President Trump issued an executive order blocking the Chinese-controlled photonics firm HieFo from acquiring $3 million in assets from the U.S.-based aerospace company Emcore, citing national security risks.

Federal Reserve Bank of Philadelphia President Anna Paulson said she anticipates that inflation will moderate, the labor market will stabilize, and the U.S. economy will grow by about two percent this year. She added that, “if all of that happens,” then interest rate cuts could be possible later in 2026.

Nvidia and AMD both unveiled new, more powerful AI chips at the Consumer Electronics Show in Las Vegas. Meanwhile, China reportedly told Chinese-based tech companies to pause their orders of advanced H200 chips from Nvidia.

New analysis forecasts the average national gas price to drop to $2.97 per gallon in 2026, the lowest price since 2020.

President Trump said that he will not allow defense companies to issue dividends or stock buybacks, which he said comes “at the expense and detriment of investing in Plants and Equipment” until the companies increase production efficiency.

Analyzing the data behind the U.S.’s low life expectancy.

Trader Joe’s $3 canvas tote bags have become an international fashion phenomenon, with resellers listing them for thousands of dollars. Nothing says “stylish” like paying four figures for something designed to carry frozen samosas.

Charts of the Week

I found the following articles to be of note. Some may be of interest only to advisors while others are aimed more broadly. You may hit paywalls below; many can be overcome here.

- Ten Unexpected Things 2026 May Bring (Nir Kaissar)

- Dividends by the Numbers in December 2025 and 2025-Q4 (Political Calculations)

- The Great Broadening (Matt Cerminaro)

This is the best thing I’ve read recently. The funniest. The silliest. The most terrifying. The best commercial. Permabear. “Drink Around the World.” 2025 in film and television. Italia. Roth 401(k). Financial automation.

A ticket for the college football national championship game is going to cost a lot of money. Miami hasn’t won a title in 24 years and is playing in its home stadium after spending five weeks on the road. Indiana has the largest living alumni base of any school and is new to this football thing. As I write this (on Saturday, after the semi-finals have been played), do you have a guess for the current price range, including fees? About $4,000 per seat on the low end and about $19,000 on the high end.

“The big money in booms is always made first by the public – on paper. And it remains on paper.”

~ Edwin Lefèvre

Securities and advisory services are offered through Madison Avenue Securities, LLC, a member of FINRA and SIPC, a registered investment advisor. This report provides general information only and is based upon current public information we consider reliable. Neither the information nor any opinion expressed constitutes an offer or an invitation to make an offer, to buy or sell any securities or other investment or any options, futures, or derivatives related to such securities or investments. It is not intended to provide personal investment advice and it does not take into account the specific investment objectives, financial situation, and the particular needs of any specific person who may receive this report. Investors should seek financial advice regarding the appropriateness of investing in any securities, other investment, or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investors should note that income from such securities or other investments, if any, may fluctuate and that price or value of such securities and investments may rise or fall. Accordingly, investors may receive back less than originally invested. Past performance is not necessarily a guide to future performance. Diversification does not guaranty against loss in declining markets. Additional Source – CNR Speedometers® | City National Rochdale