October 15, 2023

Volume 10, Issue 42

Weekly Recap

The major domestic equity indexes provided mixed performance last week as traders weighed inflation data against dovish signals from Federal Reserve officials. Large-cap value stocks outperformed, aided by earnings beats from Citigroup, Wells Fargo, and JPMorgan Chase. The banking giants kicked off the unofficial start to third-quarter earnings reporting season on a positive note, as their profits got a boost from higher interest rates. Small caps underperformed.

The prospect of a widening war in the Middle East following last weekend’s Hamas attacks against Israel boosted gold, energy shares, and defense stocks while weighing on airlines and cruise operators. Dialysis provider DaVita also fell sharply on reports that Novo Nordisk’s new dialysis drug, after being widely adopted to treat obesity, also demonstrated success in treating kidney disease.

Sentiment got a boost at the start of last week after Fed Vice Chair Philip Jefferson told an economics conference in Dallas that he was mindful that the rise in long-term bond yields might affect the need for future rate hikes. He also acknowledged that policymakers “have to balance the risk of not having tightened enough against the risk of policy being too restrictive.”

Dallas Fed President Lorie Logan, widely considered one of the central bank’s most hawkish policymakers, also surprised some by telling another economics conference that “there may be less need to raise the fed funds rate” because of the higher yields, although she repeated her insistence that rates would need to remain elevated.

The Wednesday release of the minutes from the Fed’s September policy meeting seemed to confirm the shift in official thinking because of higher yields. While “all agreed that rates should stay restrictive for some time,” officials also agreed that the “Fed should shift communications from how high to raise rates to how long to hold rates.” By the end of the week, federal funds futures were pricing in only a 5.7 percent chance of a rate hike at the next Fed meeting in November versus 27.1 percent the previous week, according to the CME FedWatch Tool.

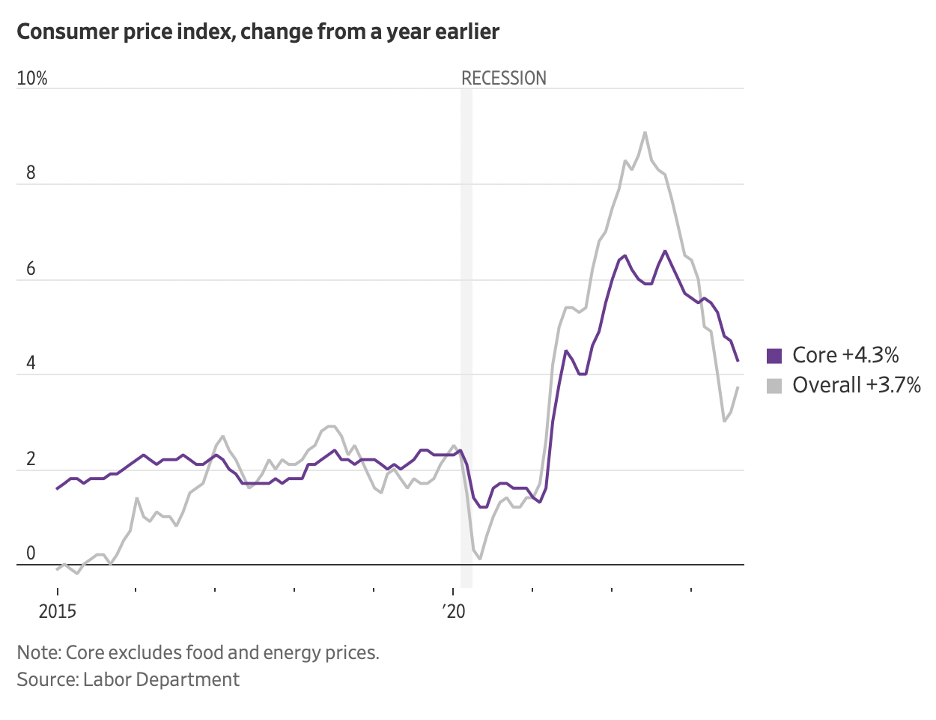

Slightly hotter-than-expected inflation readings did not seem to sway expectations for the Fed’s next move, perhaps due to expectations that officials might also weigh the added uncertainty from the war between Hamas and Israel. On Wednesday, the Labor Department reported that core (ex-food and energy) producer prices rose 0.3 percent in September, a tick above expectations. The surprise 2.7 percent increase in year-over-year core producer prices was the highest level since May, however, due to a significant upward revision in the previous month. Core CPI inflation data, released Thursday, was in line with expectations, rising 4.1 percent for the year ended September 30, its slowest pace in two years.

U.S. Treasury yields decreased sharply over much of last week, eased down by both the Fed comments and a flight to quality following the outbreak of war in the Middle East.

Market Monitor

A full listing of market performance data is available here.

DQYDJ.com (“Don’t Quit Your Day Job”) offers helpful investment calculators here, including one that shows total returns for individual stocks.

Koyfin.com provides reams of data on individual stocks, including the ability to track total return — and just about anything else — over time.

In the News

Recent progress bringing inflation down stalled in September, offering the latest sign that the path to fully extinguishing price pressures remains bumpy.

Federal Reserve officials have signaled that they could be done raising short-term interest rates if long-term rates remain near their recent highs and inflation continues to cool.

A surge in bond yields has interrupted the 2023 stock rally, leaving investors sifting through market signals to predict what comes next. Bond yields affect everything in markets and the economy, from corporate borrowing costs to the present value of future earnings and the likely direction of stock indexes.

The International Monetary Fund is upgrading its forecasts for U.S. economic growth this year and next year, while leaving its expectations for the global economy largely unchanged.

The autumn bond rout is challenging Wall Street’s longstanding belief that the U.S. government can’t sell too much U.S. Treasury paper.

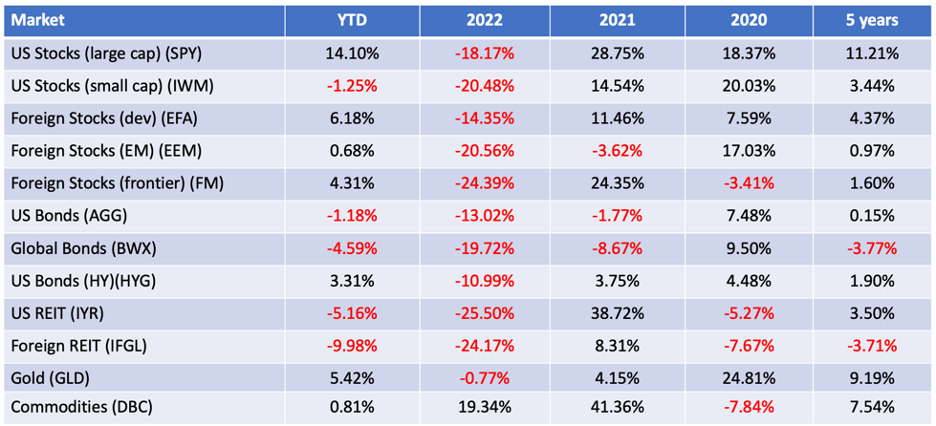

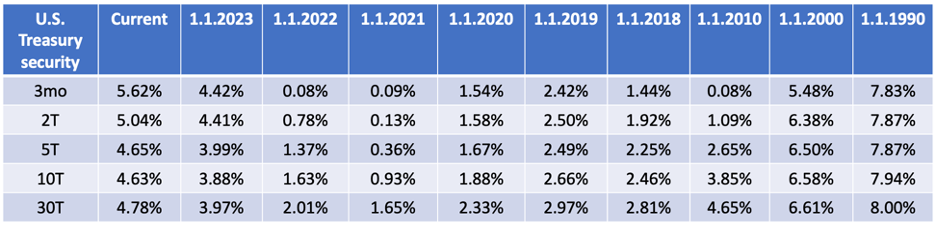

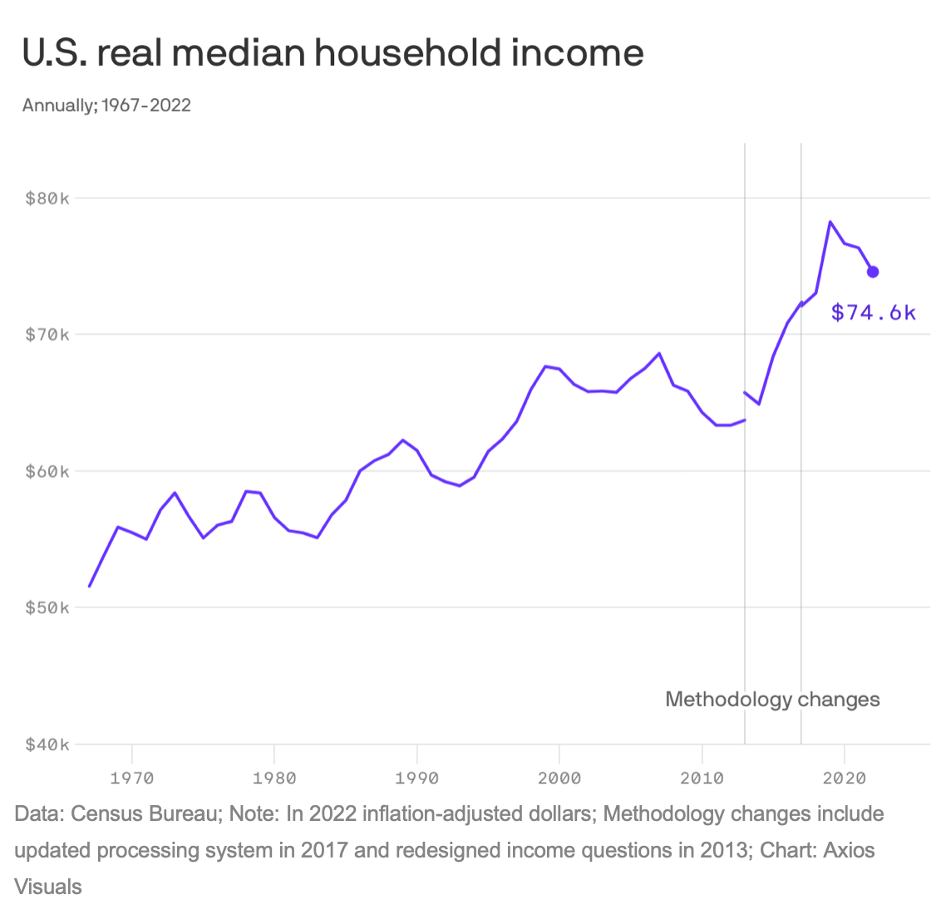

Charts of the Week

Good Reads

I found the following articles to be of note. Some may be of interest only to advisors while others are aimed more broadly. You may hit paywalls below; most can be overcome here.

The Madison Investment Quarterly magazine was published recently. It is available here.

- Investing Has Been Ugly. Stick With It Anyway. (Jeff Sommer)

- Worst U.S. Bond Selloff Since 1787 Marks End of Free-Money Era (Ye Xie)

- The Excitement, Danger, and Unknown of Small-Cap Investing’s Comeback (Michael Thrasher)

This is the best thing I read last week. The saddest. “The most interesting. The most incredible. The most absurd (details here). Not wrong. Yikes. Brazen thieves. Ingenious thief. Has Google peaked?

The amount, on average, families spend per child for after-school activities each year, is $731, according to a LendingTree survey. Spending on sports, coding classes, music lessons and other pursuits has risen not just because of inflation, but the need to stand out among peers when applying for college.

“History is the ship carrying living memories to the future.”

~ Stephen Spender

Securities and advisory services are offered through Madison Avenue Securities, LLC, a member of FINRA and SIPC, a registered investment advisor.

This report provides general information only and is based upon current public information we consider reliable. Neither the information nor any opinion expressed constitutes an offer or an invitation to make an offer, to buy or sell any securities or other investment or any options, futures, or derivatives related to such securities or investments. It is not intended to provide personal investment advice and it does not take into account the specific investment objectives, financial situation, and the particular needs of any specific person who may receive this report. Investors should seek financial advice regarding the appropriateness of investing in any securities, other investment, or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investors should note that income from such securities or other investments, if any, may fluctuate and that price or value of such securities and investments may rise or fall. Accordingly, investors may receive back less than originally invested. Past performance is not necessarily a guide to future performance. Diversification does not guaranty against loss in declining markets.