October 22, 2023

Volume 10, Issue 43

Weekly Recap

Geopolitical concerns, tough talk from Federal Reserve officials, and a rise in long-term bond yields to new 16-year highs weighed on sentiment last week to drive the S&P 500 to its biggest weekly decline in a month. The Nasdaq Composite fared worst among the major benchmarks and nearly moved back into bear market territory, ending the week 19.91 percent below its early-2022 intraday highs. Relatedly, growth stocks lagged their value counterparts. Real estate got hammered.

Stocks opened last week strongly, marking the 15th straight Monday of gains for the S&P 500, seemingly aided by limited negative news flow regarding the Middle East over the previous weekend. Deepening tensions later in the week appeared to drain the gains, however. In particular, shares fell sharply on Thursday afternoon following reports that a U.S. Navy destroyer had shot down a cruise missile apparently headed toward Israel. Reports of a drone attack on a U.S. base in Iraq further weighed on sentiment.

Last week’s “Fedspeak” was arguably less dovish than recent remarks from policymakers, added to concerns. Richmond Fed President Thomas Barkin told a real estate conference in Washington that he was “still looking to be convinced” that demand was slowing and cooling inflation. In comments before the Economic Club of New York on Thursday, Fed Chair Jerome Powell seemed to give a brief boost to sentiment after acknowledging “a clear tightening in financial conditions,” but markets pulled back sharply after Mr. Powell stated that he saw no signs that the current stance of Fed policy would push the economy into a recession.

Some upside economic surprises may have reinforced worries that rates would remain “higher for longer.” On Tuesday, the Commerce Department reported that retail sales rose 0.7 percent in October, roughly double consensus expectations. The increase was particularly strong among online retailers and at restaurants and bars, indicating continued strength in discretionary spending. Over the preceding 12 months, however, sales rose 3.8 percent, roughly in line with consumer inflation. Meanwhile, weekly jobless claims surprised on the downside, falling below 200,000 for the first time since January.

Commerce data showed the industrial side of the economy remained considerably weaker, however. Overall industrial production picked up by 0.3 percent in September but remained roughly flat over the preceding year (up 0.8%). The housing sector also demonstrated the impact of rising rates, as well as the tight labor supply. September housing starts rose more than expected, but building permits, a more forward-looking gauge, fell 4.4 percent in the month, the sharpest decline in 10 months.

Yields on the benchmark 10-year U.S. Treasury note nearly touched 5 percent in intraday trading at the end of the week, reaching its highest level since July 2007. Long-bonds also exceeded 5 percent yield and stayed there. Prices fell across the yield curve except for the shortest maturities.

Market Monitor

A full listing of market performance data is available here.

DQYDJ.com (“Don’t Quit Your Day Job”) offers helpful investment calculators here, including one that shows total returns for individual stocks.

Koyfin.com provides reams of data on individual stocks, including the ability to track total return — and just about anything else — over time.

In The News

Continued strong economic growth could hamper efforts to curb inflation, Federal Reserve Chairman Jerome Powell said in a speech on Thursday. “Additional evidence of persistently above-trend growth, or that tightness in the labor market is no longer easing, could put further progress on inflation at risk and could warrant further tightening of monetary policy,” he said. Though the Fed has signaled it probably won’t raise interest rates yet again at its next policy meeting in a few weeks, it is leaving the option open, in case additional hikes are needed to bring inflation back to its 2 percent goal. Environmental protesters disrupted the start of the speech, prompting security to escort Powell out of the room while they removed the disturbance.

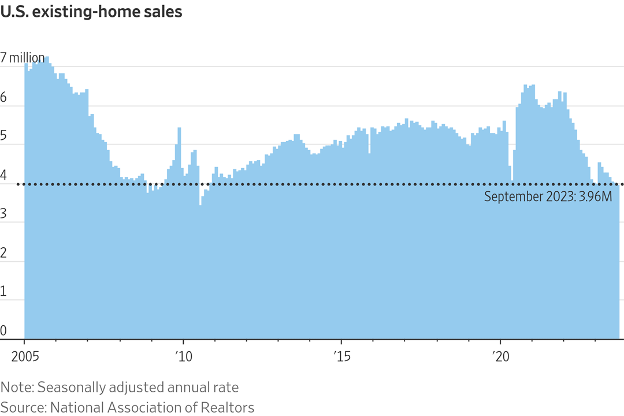

Home sales fell in September to the lowest rate in 13 years, showing the corner of the economy most weakened by high interest rates remains in decline.

Mortgage rates have hit a fresh two-decade high. The average rate on the standard 30-year fixed mortgage jumped to 7.63 percent, according to mortgage-finance giant Freddie Mac.

U.S. businesses are hanging on to workers in a still-strong labor market. Jobless claims, a proxy for layoffs, fell by 13,000 last week to the lowest level since January, according to the Labor Department.

Interest rates are high, inflation remains elevated and pandemic savings are dwindling. Yet the American consumer is on a spending binge.

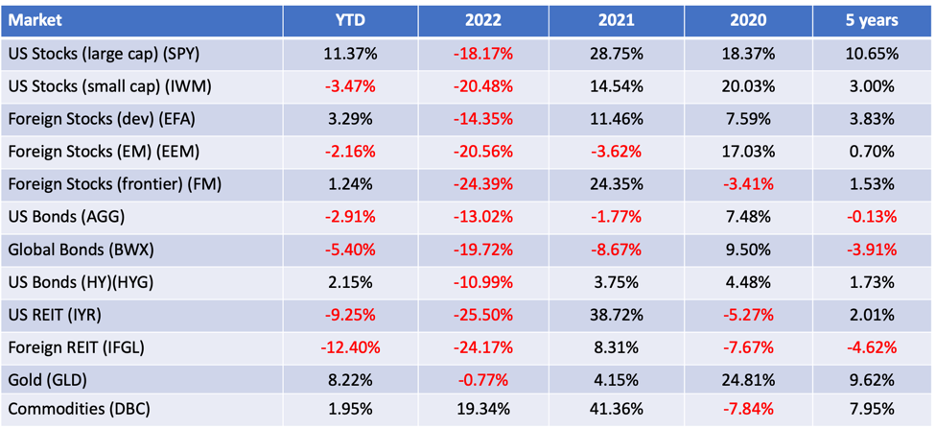

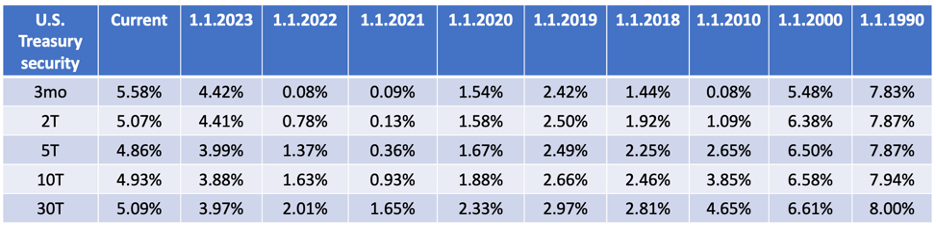

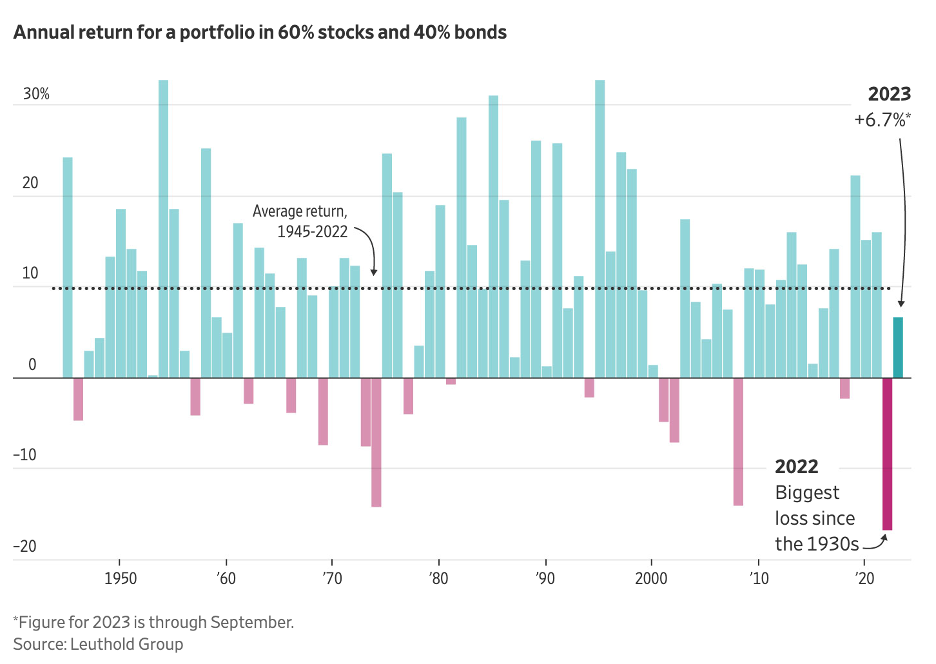

Charts of the Week

Good Reads

I found the following articles to be of note. Some may be of interest only to advisors while others are aimed more broadly. You may hit paywalls below; most can be overcome here.

- The Trusted 60-40 Investing Strategy Just Had Its Worst Year in Generations (Eric Wallerstein)

- Inflation-Proof Your Retirement Savings Now (Laura Saunders)

- Check Before Leaving (Adam M. Grossman)

How the largest RIAs are investing.

One list of the 15 best investment books of all-time (I contributed to #7).

This is the best thing I saw last week. The smartest. The saddest (also sad). The coolest. The most incredible. The most insightful. The most practical. Gorgeous. Buried the lede.

A Danish man visited every country in the world without ever taking a plane recently returned home — by boat, of course — after 10 years of travel. On his journey, he withstood visa travails, a bout of malaria, and getting trapped in Hong Kong during the pandemic. Perhaps most impressive was his living on $20 a day.

“The primary aim of human judgment is not accuracy but the avoidance of paralyzing uncertainty.”

~ Lewis Wolpert

Securities and advisory services are offered through Madison Avenue Securities, LLC, a member of FINRA and SIPC, a registered investment advisor.

This report provides general information only and is based upon current public information we consider reliable. Neither the information nor any opinion expressed constitutes an offer or an invitation to make an offer, to buy or sell any securities or other investment or any options, futures, or derivatives related to such securities or investments. It is not intended to provide personal investment advice and it does not take into account the specific investment objectives, financial situation, and the particular needs of any specific person who may receive this report. Investors should seek financial advice regarding the appropriateness of investing in any securities, other investment, or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investors should note that income from such securities or other investments, if any, may fluctuate and that the price or value of such securities and investments may rise or fall. Accordingly, investors may receive back less than originally invested. Past performance is not necessarily a guide to future performance. Diversification does not guarantee against loss in declining markets.