December 10, 2023

Volume 10, Issue 50

Weekly Recap

A late rally helped the major domestic equity indexes end last week flat to modestly higher. The small-cap Russell 2000 outperformed the S&P 500 for the third time in the past four weeks, narrowing its significant underperformance for the year-to-date period a bit. Growth stocks built modestly on their lead over value shares, however. Within the S&P, energy stocks lagged as domestic oil prices fell below $70 per barrel for the first time since June.

Continuing enthusiasm over the potential of generative artificial intelligence appeared to be one factor in boosting the growth indexes and the technology-heavy Nasdaq Composite. Shares of Google parent Alphabet rose over 5 percent on Thursday after the company revealed its new AI model, Gemini, which can process text, code, audio, images, and video and can be incorporated into mobile applications. Meanwhile, Advanced Micro Devices rose nearly 10 percent on the same day after it announced the launch of a new generation of AI chips. Earlier in the week, Apple once again moved above the $3 trillion in market capitalization line and moved back near its summer all-time highs.

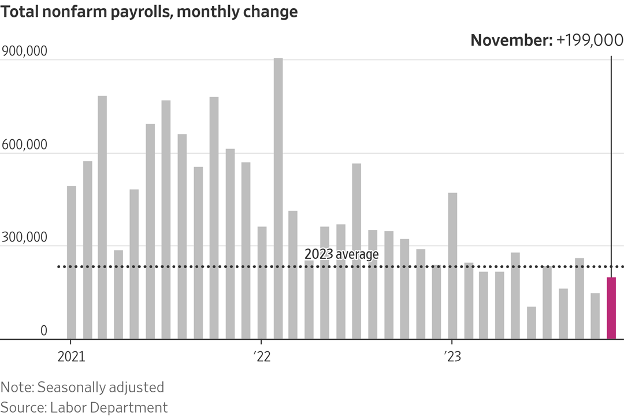

Last week’s busy economic calendar was another major driver of sentiment. Friday’s closely watched nonfarm payrolls report surprised modestly on the upside, with employers adding 199,000 jobs in November versus consensus expectations of around 180,000. The unemployment rate also surprised by falling back to 3.7 percent from a two-year high of 3.9 percent (which is still very low historically) in October. Average hourly earnings rose 0.4 percent, above expectations, but the year-over-year increase remained at a consensus 4.0 percent.

The bigger surprise – and the bigger market reaction – seemed to be the University of Michigan’s preliminary gauge of consumer sentiment in December, which jumped to its highest level since August on calming inflation fears. Survey respondents expected prices to increase by 3.1 percent in the coming year, down sharply from 4.5 percent in November and the lowest rate since March 2021. Gauges of consumer expectations and their assessment of current economic conditions also rose considerably.

The rest of the week’s economic data were mixed. On Tuesday, data from both S&P Global and the Institute for Supply Management showed a modest pickup in services sector activity in November, but the Labor Department’s count of October job openings fell much more than expected to 8.73 million, the lowest level since March 2021. October factory orders, which were reported Monday, also fell more than expected.

The data on job openings, in particular, seemed to drive a continued decrease in long-term interest rates over much of the week, with the yield on the benchmark 10-year U.S. Treasury note hitting an intraday low of 4.10 percent on Thursday. Yields rebounded higher in the wake of the payrolls report, however.

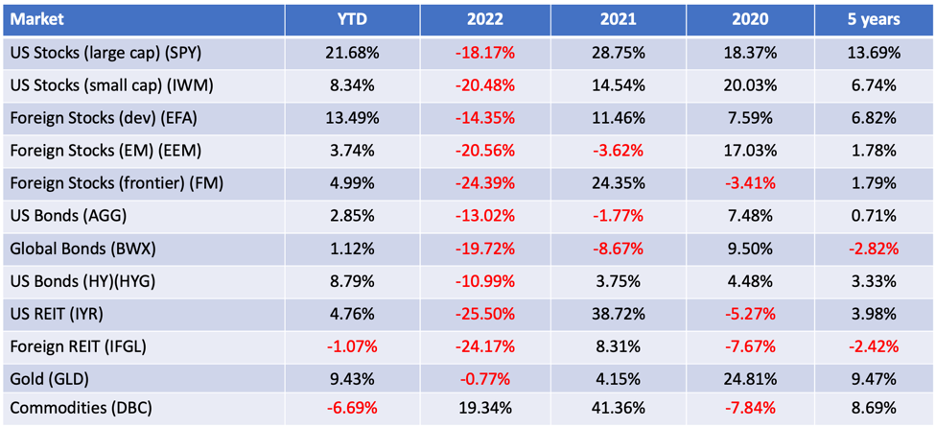

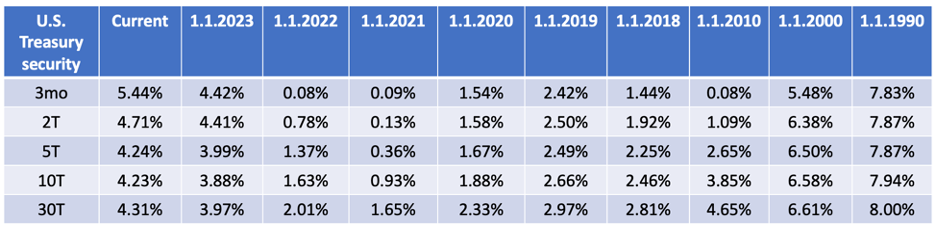

Market Monitor

A full listing of market performance data is available here.

DQYDJ.com (“Don’t Quit Your Day Job”) offers helpful investment calculators here, including one that shows total returns for individual stocks.

Koyfin.com provides reams of data on individual stocks, including the ability to track total return — and just about anything else — over time.

In The News

Employers added a seasonally adjusted 199,000 jobs last month, the Labor Department reported Friday, slower than earlier in the year but consistent with gains before the pandemic. When excluding the effects of auto-worker strikes in recent months, November’s job gain was roughly 169,000, slightly cooler than 180,000 in October. Most recent hiring occurred in two big sectors: healthcare and the government. The unemployment rate declined to 3.7 percent.

The hot labor market that underpinned a surprisingly strong economy this year is showing signs of cooling. The number of available jobs at the end of October was the lowest since March 2021, the Labor Department announced Tuesday. Fewer openings come as the unemployment rate has edged higher this year and Americans are taking longer to find new jobs.

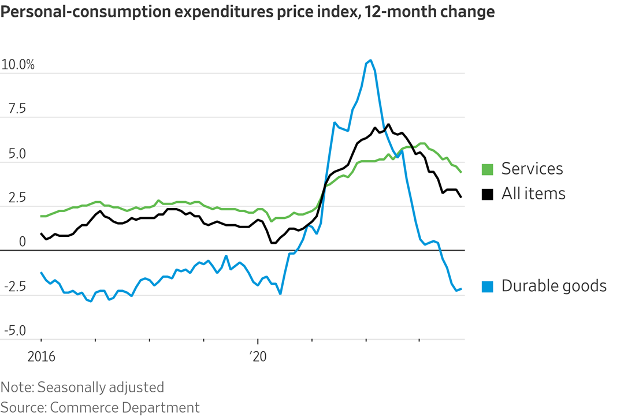

After a historic run-up in inflation, Americans are now starting to see something they haven’t in three years: deflation. To be sure, deflation—that is, falling prices—is largely confined to appliances, furniture, used cars and other goods. Economywide deflation, when prices of most goods and services continuously fall, isn’t in the cards. But economists say goods prices likely have further to fall, which will ease inflation’s return to the Federal Reserve’s 2 percent target, perhaps as early as the second half of next year.

The Labor Department on Thursday said initial jobless claims last week inched up to 220,000 from 219,000 a week earlier. First-time claims, a proxy for layoffs, are close to their pre-pandemic level and suggest that employers are holding on to workers.

U.S. mortgage rates fell to their lowest level in about four months. The average rate on the standard 30-year fixed mortgage fell to 7.03 percent last week, according to mortgage-finance giant Freddie Mac, the lowest since the week of August 10. Mortgage rates tend to loosely follow the yield of the 10-year U.S. Treasury note, which has been on the decline after softer-than-expected economic data this month.

Most of Wall Street thinks inflation has been conquered. There is a lot at stake if they are wrong.

Charts of the Week

Good Reads

I found the following articles to be of note. Some may be of interest only to advisors while others are aimed more broadly. You may hit paywalls below; most can be overcome here.

- Signs of a weakening job market, in five charts (The Wall Street Journal)

- Don’t Put Your Eggs in One Basket. That Investing Principle Still Holds. (Jeff Sommer)

- Life And Money: Seven Lessons For 2024 (Daniel Crosby)

- Why Bonds Are Making a Huge Comeback (Sarah Hansen)

This is the best thing I read in the last week. The scariest. The sweetest. The saddest. The coolest. The hardest to believe. The most heartwarming. The most dangerous. The most sensible. The best thread. Rock on. Twenty first times. Horror story. The “capability gap.”

In 1996, about 8,000 firms were listed in the U.S. stock market. Since then, the national economy has grown by nearly $20 trillion. The population has increased by 70 million people. And yet, today, the number of American public companies stands at fewer than 4,000.

“There are two kinds of people who lose a lot of money: those who know nothing and those who know everything.”

~ Henry Kaufman

Securities and advisory services are offered through Madison Avenue Securities, LLC, a member of FINRA and SIPC, a registered investment advisor.

This report provides general information only and is based upon current public information we consider reliable. Neither the information nor any opinion expressed constitutes an offer or an invitation to make an offer, to buy or sell any securities or other investment or any options, futures, or derivatives related to such securities or investments. It is not intended to provide personal investment advice and it does not take into account the specific investment objectives, financial situation, and the particular needs of any specific person who may receive this report. Investors should seek financial advice regarding the appropriateness of investing in any securities, other investment, or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investors should note that income from such securities or other investments, if any, may fluctuate and that price or value of such securities and investments may rise or fall. Accordingly, investors may receive back less than originally invested. Past performance is not necessarily a guide to future performance. Diversification does not guaranty against loss in declining markets.