December 17, 2023

Volume 10, Issue 51

Weekly Recap

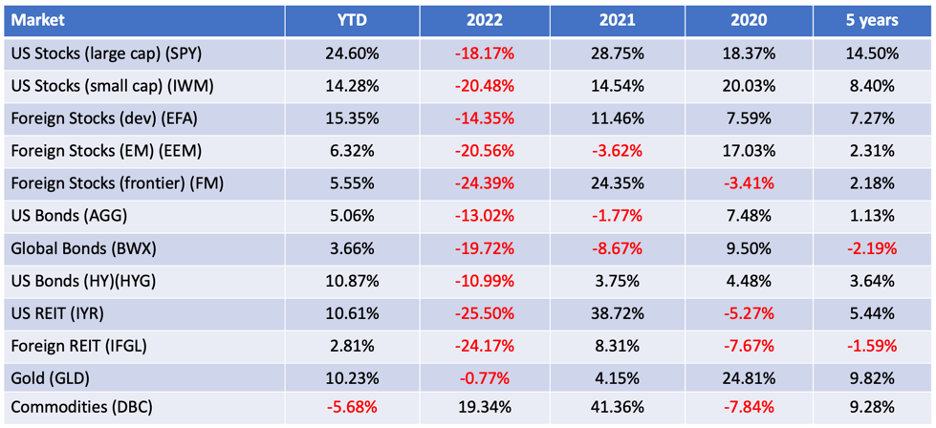

The S&P 500, the Nasdaq Composite, and Dow Jones Industrial Average recorded their seventh consecutive weeks of gains through Friday, the longest such streak for the S&P since 2017. The gains lifted the first two benchmarks to 52-week highs and the Dow to an all-time record. Continuing a recent pattern, the week’s gains were also broadly based. An equally weighted index of S&P 500 stocks outpaced its market-weighted counterpart by 131 basis points. Small-caps also outperformed, and the 5.55 percent surge in the Russell 2000 lifted it out of bear market territory (down 20% or more) for the first time in over 20 months.

Trading volumes were elevated at the end of the last week, with the number of shares exchanging hands daily hitting a new high for 2023. Traders seemed to favor stocks with the largest short interest – in other words, those that other traders had previously bet would go down. In addition, the CBOE Volatility Index, Wall Street’s so-called “fear gauge,” fell to its lowest level in the post-COVID era.

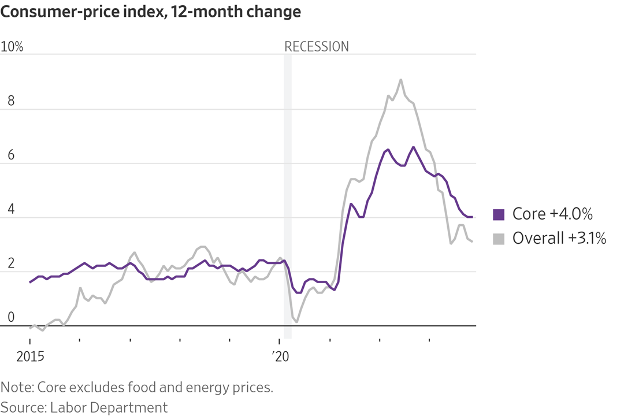

The primary factor driving sentiment appeared to be a more benign inflation environment in the eyes of both traders and policymakers. Tuesday’s report on consumer price inflation was roughly in line with estimates, with core (ex-food and energy) inflation staying steady at a year-over-year rate of 4.0 percent.

Wednesday’s producer price inflation report surprised modestly on the downside, with core inflation running at 2.0 percent for the year, a tick below expectations and its lowest level since January 2021.

Stocks had their biggest advance of the week in the wake of the report on Wednesday, which also corresponded with the Federal Reserve’s final policy meeting of the year. Officials left rates unchanged, as expected, but the quarterly “dot plot” summarizing individual policymakers’ rate expectations indicated that the median projection was for 75 basis points of rate cuts coming in 2024, up from the 50 basis points of easing in their previous projection.

Traders also seemed encouraged that Fed Chair Jerome Powell did not appear to push back on futures markets’ pricing of aggressive cuts next year in his post-meeting press conference.

Retail sales data on Thursday arguably disrupted the disinflation narrative, but traders appeared to take it in stride. Retail sales unexpectedly rose 0.3 percent in November, while October’s decline was revised lower, suggesting a strong start to the holiday shopping season. Online sales and sales at restaurants and bars were particularly strong, indicating resilience in discretionary spending. Other data released during the week indicated some surprising weakness in the manufacturing sector, however.

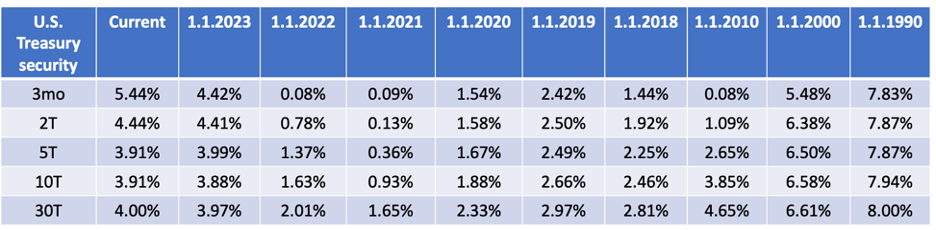

Longer-term U.S. Treasury yields fell sharply on the inflation data and Fed signals last week, bringing the yield on the benchmark 10-year U.S. Treasury note below 4 percent for the first time since the end of July.

Market Monitor

A full listing of market performance data is available here.

DQYDJ.com (“Don’t Quit Your Day Job”) offers helpful investment calculators here, including one that shows total returns for individual stocks.

Koyfin.com provides reams of data on individual stocks, including the ability to track total return — and just about anything else — over time.

In The News

The consumer-price index rose 3.1 percent in November from a year earlier, a slight slowdown from October, the Labor Department announced. Prices were up 0.1 percent from the prior month, stronger than the steady reading economists had expected. That likely means the victory dance on inflation will have to wait. Inflation has stabilized this year but is still above pre-pandemic levels, tempering hopes for near-term Federal Reserve rate cuts and maintaining price and interest-rate pressures on weary Americans.

Signaling a strong start to the holiday season, retail sales rose a seasonally adjusted 0.3 percent in November from the month before, the Commerce Department announced Thursday. That was a rebound from October’s 0.2 percent decline and a surprise to economists who had expected sales to fall again last month. This surprise increase dispelled lingering pessimism about the economy and reinforced growing sentiment that the U.S. will beat inflation without paying the price in significantly weaker growth.

The Fed held its benchmark federal-funds rate steady at a 22-year high on Wednesday and offered every reason to think that its most recent increase this past July marked the end of the most aggressive cycle of hikes in four decades. At a press conference, Fed Chair Jerome Powell focused instead on the risk of causing unnecessary harm to the economy by leaving rates too high as inflation falls.

Inflation has fallen faster this year than many Federal Reserve officials anticipated after a rapid-fire series of increases that brought interest rates from near zero to a 22-year high. The big questions now are about when the Fed can start cutting rates and by how much.

The average rate on the standard 30-year fixed mortgage fell to 6.95 percent, according to mortgage-finance giant Freddie Mac. Rates dropped below 7 percent for the first time since August.

Look at the math: It is now less affordable than any time in recent history to buy a home.

U.S. jobless claims fell last week and remain at historically low levels, suggesting that companies are holding onto workers as the economy chugs along. First-time claims, a proxy for layoffs, dropped by 19,000 to 202,000, the Labor Department announced, their lowest level since October.

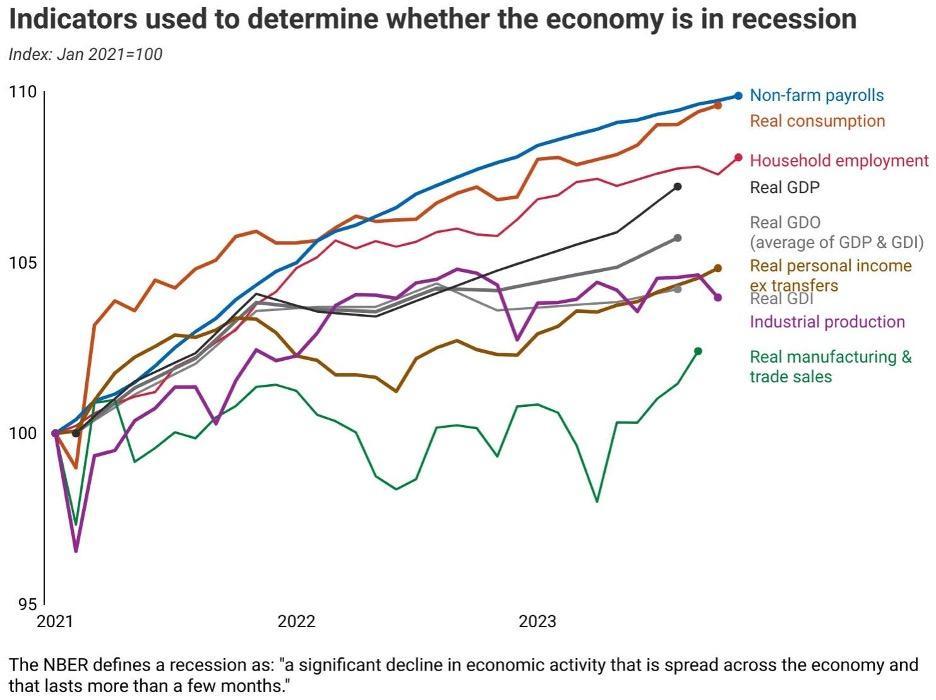

Charts of the Week

Good Reads

I found the following articles to be of note. Some may be of interest only to advisors while others are aimed more broadly. You may hit paywalls below; most can be overcome here.

- Climbing the Maturity Wall of Worry (Stanhope & Livermore)

- What Happens After a 20% Up Year in the Stock Market? (Ben Carlson)

- The Era of Easy Money Is Over. That’s a Good Thing. (Rogé Karma)

This is the best thing I’ve read in the last week; this is the best thing I saw. The scariest. The soberest. The coolest. The loveliest. The most important. The most interesting. The most astonishing. Spot on. True. Not wrong.

For forty years, PNC Financial Services has calculated the cost of purchasing the items in the classic song, The Twelve Days of Christmas. This year, prices increased by 2.7 percent over last year for a total of $46,729.86. Buying all 364 gifts repeated throughout the entire song would cost $201,972.66. Two turtle doves increased by 25 percent; however, the price of four calling birds stayed the same.

“Luck is a very thin wire between survival and disaster, and not many people can keep their balance on it.”

~ Hunter S. Thompson

Securities and advisory services are offered through Madison Avenue Securities, LLC, a member of FINRA and SIPC, a registered investment advisor.

This report provides general information only and is based upon current public information we consider reliable. Neither the information nor any opinion expressed constitutes an offer or an invitation to make an offer, to buy or sell any securities or other investment or any options, futures, or derivatives related to such securities or investments. It is not intended to provide personal investment advice and it does not take into account the specific investment objectives, financial situation, and the particular needs of any specific person who may receive this report. Investors should seek financial advice regarding the appropriateness of investing in any securities, other investment, or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investors should note that income from such securities or other investments, if any, may fluctuate and that price or value of such securities and investments may rise or fall. Accordingly, investors may receive back less than originally invested. Past performance is not necessarily a guide to future performance. Diversification does not guaranty against loss in declining markets.